Smart Benchmarks

Why have a benchmark?

Having a medium- or long-term reference allocation, a multi-assets composite benchmark, makes it possible to structure the portfolio, frame any tactical allocation decisions, and measure their added value.

What is the best benchmark for you?

It is the optimal allocation between the different asset classes that you would choose if you were forced to remain completely passive.

The concept of Smart Benchmark

Once the basic strategic allocation has been determined by the acceptable level of risk (allocation between equities, bonds, and cash), exposure to asset classes can be optimized according to the following principles:

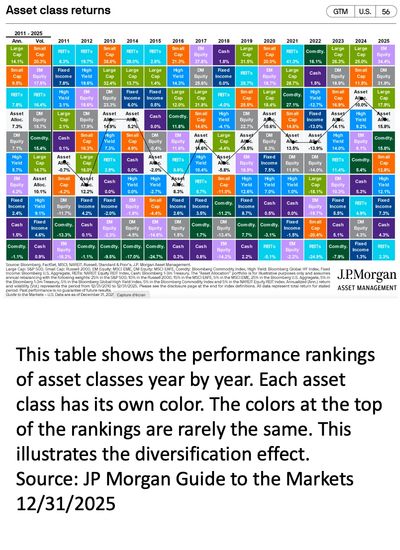

1/ Diversification across multiple asset classes with low correlation between them improves the risk/return ratio of the portfolio as a whole. For example, having structural exposure to gold, commodities, real estate, emerging market bonds, etc.

2/ Take asset class valuations into account by investing more in cheap asset classes and less in expensive ones, betting on a return to historical average valuations within 5-7 years.

3/ As correlations and valuations change over time, the smart benchmark must be reviewed every 2-3 years, which is why we refer to dynamic medium-term strategic allocation, as opposed to short-term tactical allocation (3-12 months).

Feasibility for an individual investor

Individual investors can now find inexpensive or even free simulation, analysis, and monitoring tools (ETF portfolios) online. Previously, these techniques were only available to institutional investors.