Currency Risk

Should currency risk always be hedged?

Currency risk is not remunerated over long periods, as currencies fluctuate widely around their purchasing power parity. However, hedging currency risk (via forward exchange contracts or hedged ETFs) can be costly: the interest rate differential between the two currencies (e.g., 1-year USD rate of 3.5% and EUR rate of 2% ==> hedging cost = 1.5% over 1 year).

Not in equities

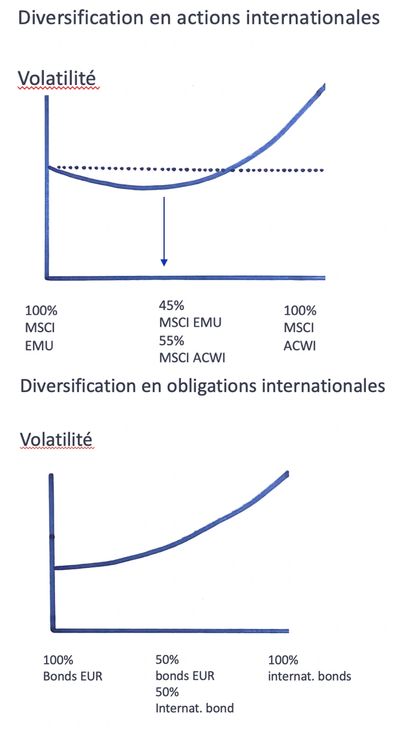

The benefits of diversifying into international equities are significant and offset all or part of the volatility of exchange rates. In addition, companies in a country whose currency is depreciating become more competitive in terms of exports and see their profits increase as a result of repatriating profits made abroad.

The currency risk associated with international equities should therefore not be systematically hedged.

Yes in bonds

The government bond markets of developed countries are far too correlated with each other. When long-term rates rise or fall in the United States, European long-term rates move in the same direction. Diversification into international bonds only adds volatility due to currency fluctuations. Only emerging market bonds denominated in local currencies offer sufficient hedging power.

For investors whose base currency is the euro, it is recommended that the majority of their bond investments be in euros. This does not preclude occasional tactical bets to take advantage of currency appreciation.